What's Inside?

In a fast-paced world where financial independence and a secure future are paramount, finding the right investment strategy becomes a crucial undertaking. Amidst a wide array of investment choices, Systematic Withdrawal Plans (SWP) stand out as an effective strategy. They provide a convenient method for individuals to receive a consistent stream of income while safeguarding the worth of their investments. Whether you are planning for your retirement, funding higher education, or seeking a regular source of income, SWPs have become an increasingly popular choice for savvy investors. Here we delve into the intricacies of SWPs, examining how they work, the potential benefits and drawbacks, and who would benefit most from this innovative investment approach.

What Is a Systematic Withdrawal Plan?

A Systematic Withdrawal Plan (SWP) is a financial investment strategy that allows an individual to withdraw a predetermined amount regularly from their mutual fund or investment portfolio. Unlike a lump sum withdrawal, SWPs provide a systematic and steady income stream. The investor specifies the frequency and amount of withdrawals, ensuring a regular flow of funds to meet their financial needs or goals. SWPs are particularly popular among retirees or those seeking a consistent source of income while keeping their investments intact and potentially growing.

How Does a SWP Work?

An SWP, or Systematic Withdrawal Plan, functions by enabling investors to regularly withdraw a set amount from their mutual fund investments over specified intervals. Here’s how it typically works:

Determine Withdrawal Amount: The investor decides on the amount they wish to withdraw periodically. This can be a fixed amount or a percentage of their total investment.

Choose Withdrawal Frequency: The investor selects the frequency of withdrawals, such as monthly, quarterly, or annually, based on their financial needs.

Set Withdrawal Instructions: The investor provides instructions to the mutual fund company regarding the withdrawal amount, frequency, and the bank account where the funds should be deposited.

Calculation of Units: When an SWP is initiated, the mutual fund company calculates the number of units to be redeemed based on the withdrawal amount and the prevailing Net Asset Value (NAV) of the fund.

Redemption Process: The mutual fund company sells the required number of units from the investor’s holdings to fulfill the withdrawal request. The proceeds from the redemption are then transferred to the investor’s specified bank account.

Continued Investment: After each withdrawal, the investor’s remaining mutual fund units continue to stay invested, potentially giving the opportunity for future growth.

Monitoring and Adjustments: The investor should regularly review their investment performance, withdrawal amounts, and adjust them as needed to align with their financial goals or changing circumstances.

Planning for SWP (Systematic Withdrawal Plan)

Developing a Systematic Withdrawal Plan (SWP) demands thoughtful planning and a meticulously crafted approach. Here are some essential steps to help you plan for SWP effectively:

Financial Assessment: Begin by assessing your financial goals, risk tolerance, and cash flow requirements. Identify the purpose of the SWP, such as supplementing retirement income or funding specific expenses.

Investment Selection: Choose an appropriate mutual fund or investment portfolio that aligns with your financial objectives and risk tolerance. Ideally, opt for funds with a history of stable returns and a track record of consistent dividend payments.

SWP Amount and Frequency: Decide on the regular withdrawal amount and how often you want to make withdrawals. Finding the perfect balance is essential to fulfilling your financial requirements while ensuring your investments don’t diminish too rapidly.

Account for Inflation: Consider the impact of inflation on your withdrawals over time. Adjusting the withdrawal amount periodically can help maintain your purchasing power and keep up with rising costs.

Emergency Fund: Before starting SWP, ensure you have an adequate emergency fund in place. This fund will cover unexpected expenses and prevent you from relying solely on SWP during unforeseen circumstances.

Tax Implications: Familiarize yourself with the tax ramifications of making SWP withdrawals. Depending on your location and the nature of your investments, SWP withdrawals could be subject to taxation. It’s advisable to seek guidance from a tax consultant to ensure effective tax planning.

Monitoring and Review: Regularly review your investment performance and reassess your financial goals. Modify the Systematic Withdrawal Plan (SWP) amount or frequency as necessary, in response to alterations in your situation or market conditions.

Exit Strategy: Have a clear exit strategy in place for your SWP. If your financial goals change or if the market conditions are unfavorable, decide when and how you will stop the SWP.

Professional Advice: If you are uncertain about SWP planning or investment choices, seek advice from a financial advisor. A professional can help tailor an SWP strategy that aligns with your unique financial situation and aspirations.

Setting Up SWP (Systematic Withdrawal Plan)

Setting up a Systematic Withdrawal Plan (SWP) is a straightforward process that involves a few essential steps:

Choose the Right Investment: Begin by carefully choosing a mutual fund or investment portfolio that matches your financial objectives and comfort level with risk. Verify that the selected fund includes a Systematic Withdrawal Plan (SWP) option.

Determine Withdrawal Amount and Frequency: Decide on the amount you want to withdraw periodically and the frequency of withdrawals (e.g., monthly, quarterly, or annually). Consider your financial needs and ensure the withdrawals are sustainable over time.

Submit the SWP Application: Contact the fund house or investment platform where you hold your investments and request an SWP application form. Fill out the necessary details, including the withdrawal amount, frequency, and other relevant information.

Provide Bank Details: Provide your bank account information where you want the withdrawn amount to be deposited. This account will receive the regular payouts from the SWP.

Submit Necessary Documents: Depending on the investment platform or fund house, you may need to submit identity proof, address proof, and other documents for verification purposes.

Review and Confirm: Before finalizing the SWP, review the application form to ensure all information is accurate. Double-check the withdrawal frequency and amount to avoid any potential issues.

Activate the SWP: Submit the completed application form to the respective fund house or investment platform. Once processed and approved, the SWP will be activated, and you will start receiving regular withdrawals as per your chosen frequency.

Example of Systematic Withdrawal Plan

Let’s consider an example of a Systematic Withdrawal Plan (SWP) to better understand how it works:

Investor Profile:

Mr. Sharma, aged 60, recently retired from his job and has accumulated a corpus of INR 30 lakhs through various investments, including mutual funds, stocks, and fixed deposits. He seeks a regular income to cover his living expenses during retirement while preserving the principal amount to counter inflation and unforeseen expenses.

SWP Setup:

Mr. Sharma decides to set up an SWP with one of the mutual funds he has invested in. After careful consideration, he chooses a balanced mutual fund with a good track record and an SWP option. He plans to withdraw INR 15,000 per month to meet his expenses.

Withdrawal Process:

Mr. Sharma contacts the mutual fund house and fills out the SWP application form. He specifies the withdrawal frequency as monthly and the amount as INR 15,000. He also provides his bank account details where he wants the withdrawn amount to be credited.

SWP Execution:

The SWP is activated, and Mr. Sharma starts receiving INR 15,000 in his bank account at the beginning of each month. The mutual fund units are sold as needed to generate the required cash for the withdrawal. The number of units sold and the resulting NAV (Net Asset Value) determine the withdrawal amount each month.

Benefit and Review:

With the SWP in place, Mr. Sharma enjoys a stable income of INR 15,000 per month, helping him cover his living expenses without the worry of market fluctuations. As the mutual fund continues to invest in various assets, the potential for growth remains, which may counter inflation and enhance the overall value of his investment.

Note: The example above is for illustrative purposes only and does not consider taxes or changes in investment performance. In real-life scenarios, taxes, market fluctuations, and the choice of investments can impact the SWP outcome.

Benefits of Systematic Withdrawal Plan

Systematic Withdrawal Plans (SWPs) offer several benefits that make them an attractive investment option, particularly for individuals in or nearing retirement. Here are some key benefits of SWPs:

Steady Income: SWP ensures a consistent flow of income at expected intervals.

Flexibility: Investors can choose the withdrawal amount and frequency according to their needs.

Capital Preservation: SWP allows investors to preserve their principal amount while receiving regular payouts.

Rupee Cost Averaging: Selling a fixed amount of units ensures investors benefit from market fluctuations.

Tax Efficiency: Capital gains tax is applicable only on the withdrawn amount, potentially reducing the tax burden.

Retirement Planning: SWP is ideal for retirees who need a reliable income source during their post-employment years.

Diversification: Establishing a Systematic Withdrawal Plan (SWP) enables the distribution of investments across different funds, offering advantages in diversification.

Automatic Discipline: Helps maintain financial discipline and prevents impulsive decisions during market volatility.

Drawbacks of Systematic Withdrawal Plan

Although Systematic Withdrawal Plans (SWPs) provide various advantages, investors must be mindful of their accompanying limitations.

Market Risk: Systematic Withdrawal Plans (SWPs) are subject to market fluctuations, and if the investment portfolio’s value declines, the withdrawals could erode the principal faster, impacting the longevity of the investment.

Inadequate Returns: Systematic Withdrawal Plans (SWPs) might not yield adequate returns to keep up with inflation or address increasing expenses, particularly when the market performs poorly.

Fixed Withdrawal Amounts: Systematic Withdrawal Plans (SWPs) usually entail withdrawing set amounts of money at regular intervals. However, these fixed withdrawals might lack the adaptability required to meet evolving financial demands or sudden expenses.

Sequence of Returns Risk: The timing of market returns can significantly affect the success of an SWP. Poor returns in the initial years of withdrawals can deplete the portfolio faster, making it challenging to recover in the future.

High Transaction Costs: Regularly making withdrawals using systematic withdrawal plans (SWPs) may lead to increased transaction expenses, which could diminish the overall returns generated from the investment.

Taxation: Systematic Withdrawal Plans (SWPs) have the potential to incur tax obligations since the funds withdrawn might be liable for capital gains tax or other relevant taxes, thereby diminishing the investor’s actual income.

Potential Outliving of Assets: If the withdrawal rate is too high or the portfolio’s performance is poor, there is a risk of depleting the investment corpus prematurely, leaving the investor with inadequate funds for their future needs.

Who Should Consider SWPs?

Systematic Withdrawal Plans (SWPs) can be suitable for certain types of investors who have specific financial goals and risk profiles. Here are some individuals who should consider SWPs:

Retirees: SWPs can be particularly beneficial for retirees who are looking to create a regular stream of income from their investment portfolio during their retirement years.

Income-Oriented Investors: Investors seeking a consistent income stream from their investments without the hassle of manual withdrawals may find SWPs attractive.

Risk-Averse Investors: SWPs can be more appealing to risk-averse individuals who prefer a steady income flow rather than dealing with the volatility of the market.

Goal-Based Withdrawals: Investors with specific financial goals, such as funding education expenses or supplementing their monthly income, can use SWPs to plan and achieve those goals.

Diversified Portfolio Holders: Those with a well-diversified investment portfolio may benefit from SWPs to manage the withdrawal process efficiently, ensuring a balanced approach to income generation.

Long-Term Investors: Systematic Withdrawal Plans (SWPs) cater primarily to investors with a long-term outlook, enabling them to retain a portion of their investment for potential growth while systematically withdrawing from the remaining portion.

Individuals with Lump Sum Investments: Those who receive a significant lump sum, such as an inheritance or a retirement corpus, may opt for SWPs to manage the distribution of funds over time.

Minimizing Market Timing Risks: Investors who are concerned about market timing risks and the potential impact of market fluctuations on lump-sum withdrawals may find SWPs more appealing.

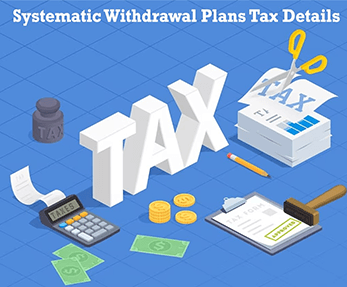

SWP Tax Details

When it comes to taxes on Systematic Withdrawal Plans (SWP), it’s important to understand the following tax details:

- Tax Deducted at Source (TDS): Unlike some other financial transactions, TDS is not applicable to SWP. This means that the mutual fund company does not deduct any tax at the time of making withdrawals.

- Capital Gains Tax: The tax treatment of SWP depends on the type of mutual fund and the holding period. Here’s how it works:

- Equity Funds: If you withdraw from an equity fund before one year, it is considered a short-term capital gain. Profits made from selling equity funds within a short period are subject to a fixed tax rate of 15%. If you hold your investment for more than one year, it is considered a long-term capital gain. Long-term capital gains from equity funds are taxed at a rate of 10% for gains exceeding Rs. 1 lakh in a financial year.

- Debt Funds: For debt funds, the tax treatment is different. If you withdraw from a debt fund before three years, it is considered a short-term capital gain. Short-term capital gains from debt funds are added to your total income and taxed as per your applicable income tax slab. If you hold your investment for more than three years, it is considered a long-term capital gain. Long-term capital gains from debt funds are taxed at a rate of 20% after adjusting for inflation using a process called indexation.

How to Start SWP?

To initiate a Systematic Withdrawal Plan (SWP), follow these simple steps:

Visit the mutual fund company’s website: Go to the official website of the mutual fund company where you have invested in a fund. Look for the SWP form and download it.

Fill in the required details: Fill in the necessary information on the SWP form. You will be asked to specify the date on which you want to make the withdrawals. You can choose to withdraw a fixed amount regularly or only withdraw the appreciation amount that your investment has gained.

Submit the form: You have the option to submit the filled-out SWP form either at the mutual fund company’s office or through an authorized agent. Some mutual fund companies also provide the convenience of submitting the form online through their website.

SWP proceeds: By default, the withdrawn amount will be credited to the bank account that you have registered with the mutual fund company. However, if you want the amount to be deposited in a different bank account, you need to provide the details of that account.

How to Stop SWP?

To stop a Systematic Withdrawal Plan (SWP), follow these simple steps:

Visit the mutual fund company’s website: Once again, go to the official website of the mutual fund company from where you initiated the SWP. Look for the form specifically designed for the cancellation of SWP and download it.

Fill in the required details: Fill in the necessary information on the cancellation form. Make sure to provide accurate details to ensure a smooth cancellation process.

Submit the form: You have the option to submit the filled-out cancellation form either at the mutual fund company’s office or through an authorized agent. Some mutual fund companies also provide the convenience of submitting the form online through their website.

Timing of submission: It’s important to submit the cancellation form at least 7 days before the date of your next scheduled withdrawal. This ensures that the cancellation is effective from the same period. If you fail to submit the form within the specified time frame, the cancellation will be applicable from the subsequent withdrawal period.

Top Myths About SWPs

SWP means guaranteed returns: One common myth about SWPs is that they guarantee consistent returns. However, SWPs are subject to market fluctuations and the performance of the underlying investments. The returns can vary depending on market conditions.

SWP is only for retirees: Another myth is that SWPs are only suitable for retirees or individuals who are no longer earning income. In truth, SWPs are open to everyone as a means of obtaining consistent earnings from their investment ventures.

SWP depletes the entire investment: There’s a perception among some individuals that choosing systematic withdrawal plans (SWPs) will lead to the gradual exhaustion of their entire investment. However, SWPs can be designed to withdraw a specific amount or a percentage of the investment, allowing the remaining principal to continue growing.

SWP is taxable on the entire amount: It is a misconception that the entire SWP amount is taxable. In fact, only the gains or profits realized from the investments are subject to taxation, not the entire withdrawn amount.

SWP is the same as regular withdrawals: SWPs are often misunderstood as being similar to regular withdrawals. However, SWPs follow a systematic and planned approach, allowing investors to withdraw a predetermined amount at regular intervals, providing a structured income stream.

SWP can only be set up for mutual funds: While SWPs are commonly associated with mutual funds, they can also be set up for other investment vehicles such as exchange-traded funds (ETFs) or individual stocks. The availability of SWPs may vary depending on the investment option.

SWP locks in investments: Certain people hold the misconception that once they start a Systematic Withdrawal Plan (SWP), their investments become fixed and unalterable. However, the truth is quite the opposite. Investors actually possess the freedom to adjust or cease the SWP according to their needs and preferences.

In conclusion, Systematic Withdrawal Plans (SWPs) can be a powerful tool for investors seeking a steady stream of income from their investments while maintaining a level of flexibility and control over their portfolio. By setting up regular withdrawals, investors can effectively manage their cash flow and address specific financial goals, such as retirement or education funding. However, it is crucial for investors to be aware of the potential drawbacks, including market risks, sequence of returns risk, and taxation implications. To make the most of SWPs, individuals should carefully assess their financial needs, risk tolerance, and long-term objectives, seeking professional advice when necessary. With prudent planning and a well-structured approach, SWPs can become a valuable component of a diversified investment strategy, providing financial stability and peace of mind for the years to come.