What's Inside?

What is Car Insurance?

Auto insurance offers financial security against car-related damages or losses, safeguarding your vehicle. It covers various risks, such as accidents, theft, or natural disasters, and helps you pay for the costs incurred due to such events. In exchange for this coverage, you pay a fee called a premium to an insurance company. There are different types of car insurance policies available, which offer varying levels of coverage and protection. It is mandatory in most countries to have at least basic car insurance to legally drive on public roads.

Key Features of Car Insurance

Car insurance has several key features that are important to understand. These include:

Coverage for damages: Car insurance protects you financially by covering damages to your car caused by accidents, theft, or natural disasters.

Third-party liability coverage: Car insurance also covers damages caused by you to other people’s property or injury to others while driving.

Policy options: There are different types of car insurance policies to choose from, including third-party, comprehensive, and own damage policies.

Premiums: Car insurance premiums are the amount you pay for the policy. Premiums can vary based on factors such as your driving history, the type of car you have, and your location.

Deductibles: A deductible is the amount you pay out of pocket before the insurance coverage kicks in. Increasing the amount you pay out of pocket before insurance kicks in may lead to decreased monthly insurance costs.

Add-ons: Car insurance policies may offer add-ons such as roadside assistance, personal accident cover, and zero depreciation cover.

No-claim bonus: If you don’t make any claims during the policy period, you may be eligible for a no-claim bonus, which can lower your premiums for the next year.

What are the Different Types of Car Insurance Policies in India?

In India, there are different types of car insurance policies that offer different kinds of coverage.

- Third-party Liability Policy: This is a must-have policy by law, which covers you against liabilities like injury, death, and property damage caused to others while driving your car.

- Own Damage Car Insurance: This policy covers damages to your own car caused by accidents, natural calamities, and other such events.

- Comprehensive Car Insurance Policy: This policy includes both the benefits of the Third-party Policy and Own Damage cover. You can also opt for additional coverages, called add-ons, to enhance your coverage further.

Car Insurance Coverage

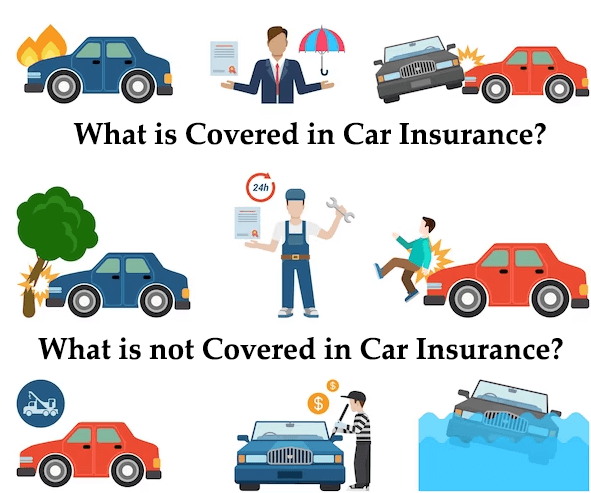

What is Covered in Car Insurance?

Your car insurance policy will offer different types of coverage depending on the type of policy you select. Third Party Car Insurance Plans cover financial liabilities you might face in case of a mishap involving your car, such as physical injury, death, or damage to property caused to a third party.

A comprehensive car insurance policy offers additional coverage for your own car, including accidental damage, fire and explosion, theft, damages from natural disasters or man-made perils like riots or strikes, in-transit damage during transportation, and personal accident cover in case you suffer an injury in an accident involving your insured car.

With a comprehensive policy, you can also rest assured that any damages suffered by third parties will be covered, and that you will receive compensation for any financial loss incurred due to theft, accidents or natural calamities.

What is not Covered in Car Insurance?

While car insurance policies provide a range of coverage, there are some things that are typically not covered under most policies. Here are some examples:

- Regular wear and tear: Car insurance policies are designed to cover unexpected events, and regular wear and tear on your car is not one of them.

- Mechanical or electrical breakdowns: Most car insurance policies do not cover mechanical or electrical breakdowns, as they are considered to be a part of normal wear and tear.

- Driving without a valid license: If you get into an accident while driving without a valid license, your car insurance policy will not cover you.

- Driving under the influence of alcohol or drugs: If you cause an accident while under the influence of alcohol or drugs, your car insurance policy may not cover you.

- Intentional damage: If you intentionally damage your own car or someone else’s car, it is unlikely that your car insurance policy will cover the damages.

- Racing or other illegal activities: Most car insurance policies do not cover damages or injuries that occur during illegal activities such as racing.

It’s important to carefully read your car insurance policy to understand what is and isn’t covered. If you have any doubts, you can always contact your insurance company to ask for clarification.

Add-On Covers for Car Insurance Policy

Add-on covers are extra benefits that can be added to your car insurance policy for an additional premium. Some of the commonly offered add-ons for car insurance policies are:

Zero Depreciation Cover – This add-on ensures that you get the full value of the replaced car parts during repairs or replacement, without considering the depreciation factor.

Roadside Assistance Cover – This add-on provides assistance in case of breakdowns, flat tyres, and other such incidents on the road.

No Claim Bonus (NCB) Protection Cover – This add-on helps you retain your NCB even after making a claim during the policy period.

Engine Protection Cover – This add-on covers damages caused to your car engine due to oil leaks, water damage, etc.

Return to Invoice Cover – This add-on helps you get the invoice value of the car in case of total loss or theft of the car.

Consumables Cover – This add-on covers the cost of consumable items like nuts, bolts, screws, etc. that are used during repairs.

Make sure to carefully assess your needs and budget before opting for any add-on cover for your car insurance policy.

Why should you buy a Car Insurance policy online?

Buying a car insurance policy online offers several benefits, including:

- Convenience: You can buy a policy from the comfort of your own home or office, at any time that is convenient for you.

- Cost-effective: Online car insurance policies are often cheaper than policies bought through agents or offline channels, as they save on overhead costs.

- Quick and easy: The entire process of buying car insurance online is quick and easy, and can be completed within a matter of minutes.

- Comparison: You can easily compare the features and benefits of different policies from different insurance providers, allowing you to make an informed decision.

- Customization: You can customize your policy according to your specific needs and requirements, by adding or removing add-on covers as necessary.

- No paperwork: Buying car insurance online eliminates the need for physical paperwork, as everything can be completed online, making it a more eco-friendly option.

Things to keep in mind while buying a car insurance policy

If you’re buying car insurance policy, here are some important things to keep in mind:

Policy Coverage: Carefully read the policy to know what it covers and what it doesn’t. Pick the right type of policy and coverage to ensure you’re protected at the time of claim.

Add-ons: Consider buying add-ons for additional benefits at a reasonable extra charge. Evaluate each add-on closely to determine which ones you need to cover your car against accidental damages.

Service Benefits: Look for policies that offer cashless garages, easy claims process, and reliable customer support.

Insured Declared Value (IDV): When buying the policy, choose an IDV that is close to your car’s market value, even though it might be more expensive. It will benefit you in the long run at the time of claim.

How to Buy/Renew Car Insurance Online

Purchase a fresh car insurance policy through online channels.

- Go to your insurance provider’s website and provide the necessary details, such as your car registration number, mobile number, and email address.

- Enter the policy details and select any add-ons you want to include.

- Complete the process by paying the premium amount online.

You will receive a confirmation email along with the policy.

To renew an existing car insurance policy online:

- Visit the insurance provider’s website and select the option to renew your policy.

- Provide the required details and choose to include or exclude any add-ons. Then, pay the premium amount online.

- The renewed policy will be sent to your registered email address.

Why Should You Renew Expired Car Insurance Immediately?

Renewing your expired car insurance is crucial because:

- Loss of NCB: If you do not renew the policy within 90 days from the expiry date, the accumulated No Claim Bonus (NCB) earned from your car insurance policy over the years shall be nullified.

- Vulnerable to fines: Driving with an expired car insurance policy can make you vulnerable to fines. The traffic penalty for driving an uninsured car can go up to Rs. 4,000 and/or imprisonment.

- Unwanted financial implications: Failing to renew your car insurance promptly could leave you without coverage. This means you might have to bear the full cost of any damages or injuries resulting from an accident, particularly if others are involved.

Key Benefits of a Car Insurance Policy

Having a car insurance policy comes with many benefits for the policyholder. Here are some key benefits:

- Legal compliance: Indian law requires all car owners to have at least a third-party car insurance policy. Failure to possess the required item may result in a penalty of Rs. 2,000 or a maximum of 3 months’ imprisonment.

- Protection against third-party liabilities: If you are in an accident and cause harm to someone else’s body or property, your car insurance policy will cover the cost of compensation. There is no limit on compensation for bodily injuries, disability, or death, but it is limited to Rs. 7.5 lakh for property damage.

- Protection against own-damages: If your car is damaged in an accident or by natural disasters, man-made disasters, fire, explosion, vandalism, etc., your insurance policy will cover the cost of repairs or replacement.

- Coverage against theft: If your car is stolen, your insurance company will pay you the market price of your car.

- Personal accident cover: You can also get a personal accident cover of up to Rs. 15 lakh with your car insurance policy, which covers you in case of death, bodily injuries, or disability caused by a car accident.

Car Insurance Claim Process

For Damages to Your Own Car:

If your car gets damaged, here’s what you need to do to claim your car insurance:

- Call your insurance company as soon as possible after the accident or damage. They will ask you to fill out a claim form and give some paperwork. You have the option to acquire the necessary forms directly from their official website.

- An insurance surveyor will come and inspect your car and make a report. You’ll get a copy of this report.

- After your car gets repaired, you need to get all the signed forms and documents from the garage and give them to the surveyor. The surveyor will send them to the insurance company.

- If the claim is approved, the insurer will provide a delivery order (DO) for cashless claims. You can pay the repair bill and take your car.

- If you paid for the repair yourself, you can submit the bill to the insurer for reimbursement. Depending on your insurance policy, you may get a refund later.

For Third Party Claims:

If someone demands compensation from you for damages that you caused, you need to let your car insurance company know. Don’t agree to anything or talk to the person until you have spoken to your insurer.

You will need to give your insurer a copy of the legal notice, as well as your driver’s license, registration certificate, and police report.

Your insurer will then review the details of the accident and assign a lawyer to represent you if everything is in order.

If the court decides that you are responsible for the damages, your insurer will pay the third party on your behalf.

For Stolen Car:

If your car is stolen, you need to do some things to make an insurance claim:

- First, you must go to the nearest police station and file an FIR to report the theft of your car.

- Then, you must give a copy of the FIR to your insurance company.

- When you receive the final police report, you need to give a copy of it to your insurance company. They will assign an investigator to the case.

- Once your insurance claim is approved, you need to submit your car’s RC book to your insurer.

- The name on the RC book will be changed to the name of the insurance company.

- Next, you need to give the replica car keys and a letter of subrogation to the insurance provider. They also require a notarized indemnification on stamp paper.

- After completing all the formalities, the insurance company will disburse the claim amount to you.

Documents Required for Filing a Car Insurance Claim

If you need to file a car insurance claim, you will need the following documents depending on the type of claim:

For accident claims:

- A copy of the car’s Registration Certificate (RC) book

- A copy of the driver’s license of the person who was driving the car at the time of the accident

- A First Information Report (FIR) filed at the police station

- Estimates for the cost of repairs from the garage

- Know Your Customer (KYC) documents

- If the accident occurred during a riot or strike, then an FIR is mandatory.

For theft claims:

- A copy of the car’s RC book and the original car keys

- An FIR filed at the police station and the final police report

- The RTO transfer papers

- KYC documents

- A Letter of Indemnity and Subrogation

Make sure to have all the necessary documents in order when filing a car insurance claim.

How to Calculate Car Insurance Premium

The price you pay for your car insurance is called the car insurance premium. There are different ways to calculate your car insurance premium:

First, you can use an online premium calculator tool provided by insurance companies. You need to enter some details like the policy coverage and add-ons you want, and the calculator will tell you the total premium you need to pay.

Second, the premium for own damage insurance is calculated using the Insured Declared Value (IDV) of your car. IDV represents the highest sum you’re eligible to receive through your insurance coverage. The premium tariff decided by the insurer, the add-ons you choose, and discounts like No Claim Bonus are also included.

Third, the IDV of your vehicle is calculated using the car manufacturer’s list price, minus the depreciation deduction, and the cost of vehicle accessories (if any) that are not included in the list price, minus the depreciation deduction of accessories.

Lastly, the premium rates for Third-Party Liability Insurance are set by the Insurance Regulatory and Development Authority of India (IRDAI). It depends on your car’s engine cubic capacity and is updated every financial year.

Factors Affecting Car Insurance Premium

Your car insurance premium is determined by several factors, including:

Your car’s Insured Declared Value (IDV) – The higher your car’s market value, the higher your premium will be.

Make and model of the car – Expensive cars and cars with high repair/replacement costs will have a higher premium.

Fuel type – Repairing diesel and CNG-fueled cars is more expensive than petrol-fueled cars, so they will have a higher premium.

Year of manufacture – Newer cars may be more expensive to insure since their spare parts may not be widely available yet.

Location – If you live in an area with high traffic density, you are at a higher risk of accidental damage, so your premium may be higher.

Claim history – A good claim history will give you a No Claim Bonus (NCB) and lower your premium.

Add-ons – The cost of add-ons will be added to your premium.

How to Get a Physical Copy of your Car Insurance Policy?

To get a physical copy of your car insurance policy, you can follow these steps:

- Contact your insurance company: You can get in touch with your insurance company’s customer service team via phone, email, or chat to request a physical copy of your policy.

- Provide your policy details: Once you connect with the customer service team, you’ll be required to provide your policy details, such as your policy number, date of purchase, and any other relevant information.

- Choose the delivery method: You can choose the delivery method that suits you the best. Your insurance company can mail the physical copy of your policy to your registered address or provide you with a printed copy at their nearest branch office.

- Verify the information: Before accepting the physical copy of your policy, make sure to verify all the information on the policy document, such as the policyholder’s name, vehicle details, policy coverage, and premium amount.

- Keep the physical copy safe: Once you receive the physical copy of your car insurance policy, make sure to keep it safe and secure as you may require it during any claims settlement process or for any other insurance-related purposes.

List of Best Car Insurance Companies in India:

Here are the top car insurance companies in India along with some of their key features:

| Insurance Company | Key Features |

| ICICI Lombard Car Insurance | 1. Comprehensive coverage

2. Cashless garage network across India 3. 24/7 customer support 4. Option to customize policy with add-ons |

| HDFC ERGO Car Insurance | 1. Comprehensive coverage

2. Wide network of cashless garages 3. Instant policy issuance and renewal 4. 24/7 customer support |

| Bajaj Allianz Car Insurance | 1. Comprehensive coverage

2. Flexible coverage options 3. Cashless garage network across India 4. Hassle-free claim settlement process |

| New India Assurance Car Insurance | 1. Comprehensive coverage

2. Personal accident coverage for driver and passengers 3. Easy claim settlement process 4. Discounts for anti-theft devices |

| National Insurance Car Insurance | 1. Comprehensive coverage

2. Personal accident coverage for driver and passengers 3. Cashless garage network across India 4. 24/7 customer support |

| Oriental Insurance Car Insurance | 1. Comprehensive coverage

2. Cashless garage network across India 3. 24/7 customer support 4. Personal accident coverage for driver and passengers |

It’s important to note that this is not an exhaustive list and there are many other car insurance companies in India that offer various features and benefits.

Important Terminologies Related to Car Insurance

Here are some important terminologies related to car insurance:

- Premium: The amount of money paid by the policyholder to the insurance company for the car insurance coverage.

- IDV (Insured Declared Value): The maximum sum assured fixed by the insurance company, which is the maximum amount payable in case of theft or total damage of the vehicle. It is calculated based on the current market value of the vehicle and the depreciation rate.

- Third-Party Insurance: This covers the policyholder’s liability towards the damages caused to a third party due to an accident involving the insured vehicle.

- Own Damage Insurance: This covers the damages caused to the policyholder’s own vehicle due to accidents, theft, fire, or natural calamities.

- No Claim Bonus (NCB): This is a discount provided by the insurance company to the policyholder for not making any claims during the policy term. It is a reward for safe driving and reduces the premium amount.

- Deductible: The amount that the policyholder has to bear before the insurance company pays the claim amount. It is a pre-agreed amount between the policyholder and the insurance company.

- Add-On Covers: These are additional covers that can be purchased by the policyholder along with the basic insurance coverage to enhance the policy’s protection. Examples of add-on covers are zero depreciation cover, engine protector, and roadside assistance.

- Cashless Garage Network: A network of garages authorized by the insurance company where policyholders can get their vehicles repaired without paying cash. The insurance provider handles the repair costs by directly coordinating with the garage.

- Claim Settlement Ratio: The percentage of claims settled by the insurance company against the total claims received during the policy term. A high claim settlement ratio indicates that the insurance company is reliable and trustworthy.

- Policy Period: The duration for which the car insurance policy is valid. It is usually one year, but some insurance companies also offer policies for two or three years.

Car insurance is an essential protection that every vehicle owner should invest in. It not only safeguards you from potential financial liabilities in the event of an accident but also ensures that you comply with legal requirements in most jurisdictions. To make the most informed decision and find the best coverage for your needs, it is crucial to compare car insurance policies from different providers. Remember, the cheapest option may not always provide the comprehensive coverage you require, so carefully assess the features, benefits, and reputation of each insurance company.

Banking Karo

Banking Karo